Global macroeconomic developments offered investors several reasons to be cheerful three months ago. But investors have become too sanguine, too quickly, about the remaining risks to future earnings, and this has been reflected in higher valuations.

The unpredictable political hurdles to be cleared in 2017 have left financial assets more susceptible than usual to a sharp correction – that is to say a fall of around 10 per cent.

Since then the run of good macroeconomic data has continued, spurring on investors who appear to have put politics and uncertainty to one side. Global equities have returned roughly 3.5 per cent in a ‘hope’-based rally, where valuations have risen without significant earnings momentum, which is unusual for this later stage in the business cycle.

Such incongruities mean that investors face the same dilemma as we enter the second quarter. On the one hand, leading global economic indicators suggest output growth is set to reach 3.75 to 4 per cent by the end of June, a rate not reached since the initial bounce-back from the financial crisis in 2009-10. Higher bond yields and rising inflation are likely to curtail growth in the second half of the year, but it seems unlikely this will be to the extent that growth will revert to anaemic levels.

On the other hand, the equity risk premium has plunged in the past four months: in the US it is near five-year lows, while in Europe it is close to three-year lows.

Investors are demanding less and less compensation for tomorrow’s uncertainties. Some analysts argue this reflects receding fears of ‘secular stagnation’. But if investors were putting to rest this thesis, upgrades to medium- and long-term growth forecasts would be expected. There has been little evidence of this.

Historically, equity markets struggle as bond yields are driven higher by expectations of inflation, but not growth. The ongoing economic expansion may help companies to navigate this threat, but equity selection is focusing more and more on pricing power: the ability of firms to pass on rising costs to their customers.

Continued expansion suggests investors should remain invested – bearing in mind that bear markets very rarely occur without recessions – but fundamental analysis warns not to become too complacent.

Risk-on/risk-off indicators show that more cautious sub-strategies are again outperforming the more belligerent, even though markets are rising overall. For example, high-volatility stocks have started to underperform low-volatility plays, and growth stocks are outperforming value stocks again. In short, despite low volatility, markets are not rewarding higher levels of risk taking.

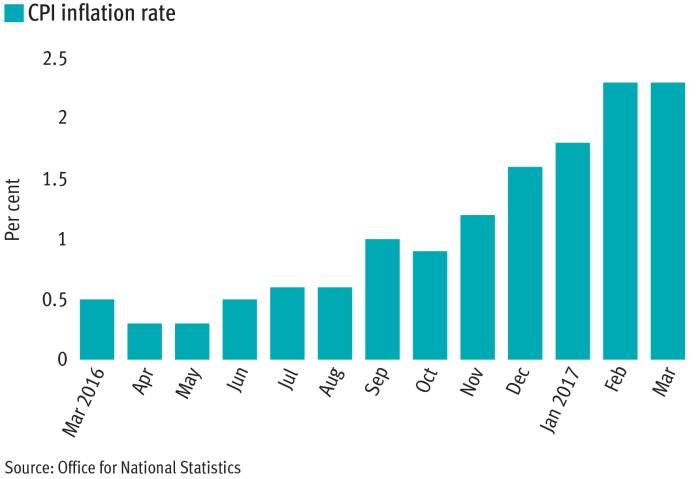

Consensus now expects the UK economy to grow at 1.5 per cent (inflation-adjusted) in 2017, a large upward revision to what is a more realistic rate from last year’s overly pessimistic forecasts.

Nevertheless, 1.5 per cent is nothing to be excited about, and despite a decent six months since the referendum, there are a number of factors that are likely to weigh on growth in the first two or three quarters of 2017.