Economic data is finally reflecting the impact of coronavirus lockdowns, as can be seen in the graph below.

Given the extent of the economic slowdown and the still uncertain duration of the crisis, we think it is too early to move to a risk-on posture.

While there have been some positive signs of lockdowns easing in certain countries, we see the rally as running too far ahead of the weak economic data.

But it is not all negative news, and the very aggressive policy responses from governments and central banks have offered up attractive risk-return asymmetries in the credit markets, especially in the US.

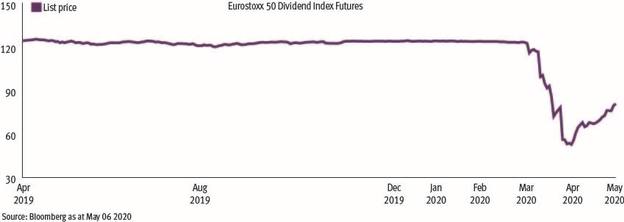

As income investors, we are of course acutely aware of the headwinds for dividend-paying equities as earnings are likely to struggle throughout the year.

The recession is also likely to drive greater dispersion among current dividend payers, while the overall level of equity income falls.

This view certainly feeds into our bias to credit overall, and highlights how a multi-asset approach to income investing offers the flexibility needed to navigate the challenges of this market environment.

But behind the dreary headlines on dividends lies a lot of nuance, and in multi-asset we work closely with our colleagues in equities to gain some clarity on the high levels of dispersion within the universe of dividend paying equities.

Even given the bleak forecasts for the global economy, Fidelity equity researchers still see 2020 dividends being maintained in 70 to 80 per cent of our exposure.

But there could be meaningful regional differences. The economies of north east Asia and Singapore have the potential to recover lost growth quicker as their management of the Covid-19 outbreak facilitates a quicker rebound in activity supporting internal demand within the region.

Companies there may not need to adjust dividend payouts, or any that do may be able to return to previous levels quickly.

Asian companies showed how nimble they could be after the great financial crisis, reducing dividends in 2009 but returning to previous payouts in 2010, in contrast to European companies that have still not returned to pre-2009 dividend levels because of economic stagnation.

Also, the longer the recession the higher the chance of insolvency, and then regulation becomes a key factor.

The US government’s bailout programme under the Coronavirus Aid, Relief, and Economic Security Act requires companies that receive help to stop paying dividends and buying back shares. France will take the same approach.

UK and European regulators appear to have been more aggressive by recently requesting that banks and some insurers stop paying dividends for a short period.

There are also major differences across sectors and companies. Some of the oil majors are well-known dividend stalwarts, and they are under significant pressure from low oil prices.

Meanwhile, some sectors will be able to maintain pricing power and could even increase revenues, such as gaming and tech companies.